As a large employer, your company will always belong to one of the contribution categories. The contribution category is determined by your company's disability risk and affects the amount of the TyEL contribution.

There are 11 contribution categories in total, with the lowest contribution category being 1 and the highest 11. Contribution category 4 is the basic category, in which the disability risk corresponds to the average level of the earnings-related pension system.

The contribution category affects the contribution as follows:

- Contribution categories 1 to 3 reduce the contribution.

- Contribution categories 5 to 11 increase the contribution.

How is the contribution category determined?

The contribution category, and therefore the disability contribution, is affected by the disability pensions of your company's employees. The contribution category is always calculated in advance for the following year on the basis of realised pension expenditure.

Pension expenditure refers to the amount of money needed to pay an employee's disability pension on average until the lowest retirement age. The amount of pension expenditure depends on the age of the employee, the amount of the pension and the duration of the disability.

The contribution category is determined by the risk ratio calculated for it. The risk ratio is calculated by comparing your company's disability pension expenditure to the average disability pension expenditure. If your company's pension expenditure is higher than the average pension expenditure, the risk ratio is higher and the contribution category is higher.

The risk ratio is calculated as the average of the risk ratios from two and three years ago. For example, the contribution category for 2026 is determined by the average of the risk ratios calculated for 2023 and 2024. It is therefore affected by the disability pension expenditure from 2023 and 2024.

What impact does the contribution category have?

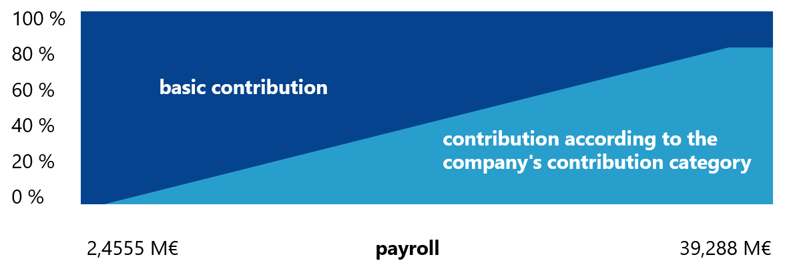

Your company's payroll has an impact on how much the contribution category affects the TyEL contribution. The higher the payroll, the higher the so-called liability level and thus the higher the impact on the disability contribution.

The liability level determines how much of the disability contribution is a basic contribution based on the age structure of the employees and how much is a contribution based on the contribution category.

In 2026, a company's liability level can range between 0–80%. If a company's liability level is 60%, for example, 60% of its disability contribution will be based on the contribution according to the contribution category. If your company's payroll exceeded EUR 39,288,000 in 2024, your company's contribution rate is 80% in 2026.

The contribution category and the liability level may change as a result of business restructuring.

View the table to see how the contribution category affects the TyEL contribution for companies of different sizes